Linear Regression in R

Given a set of noisy data points, such as the following, how can we find the best fitting linear model?

x <- c(1, 2, 3, 4, 5, 6)

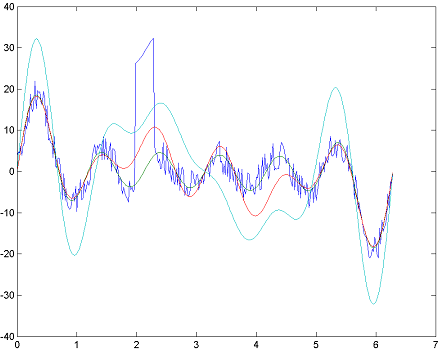

t <- seq(from = 0, by = 0.02, to = 2*pi)

A <- cbind(sin(t), sin(2*t), sin(3*t), sin(4*t), sin(5*t), sin(6*t))

e <- -4+8*runif(length(t),min=-1,max=1)

e[100:115] <- 30

y = A%*%x + e

plot(t, y, 'l')

Various packages in R support linear regression models, such as stats (for least-squares) and quantreg (for quantile regression):

library(stats)

res1 <- lm(y ~ A)

lines(t, res1$fitted.values, col='green')

qr.solve(A, res1$fitted.values)

library(MASS)

res2 <- rlm(y ~ A)

lines(t, res2$fitted.values, col='red')

qr.solve(A, res2$fitted.values)

library(quantreg)

res3 <- rq(y ~ A)

lines(t, res3$fitted.values, col='darkred')

qr.solve(A, res3$fitted.values)

How can we implement these techniques in R to better understand how they work?

Here are two implementations that use convex optimization:

# Ordinary Least Squares regression

ols <- function(x, y) {

obj <- rep(1, length(x) +2 )

obj[c(1,2)] <- 0

eye <- diag(length(x))

bvec <- y

Amat <- cbind(x, rep(1, length(x)), eye)

Dmat <- matrix(0, length(x)+2, length(x)+2)

diag(Dmat) <- 1;

Dmat[1,1] <- 1e-7

Dmat[2,2] <- 1e-7

dvec <- rep(0, length(x)+2)

res <- solve.QP(Dmat,dvec,t(Amat),meq=length(x), bvec=bvec)

yhat <- res$solution[1]*x +res$solution[2]

lines(x, yhat, col='blue')

}

# Ordinary Least Absolute Deviation regression

olad <- function(x, y) {

obj <- rep(1, length(x)+2)

obj[c(1,2)] <- 0

eye <- diag(length(x));

mat1 <- cbind(x, rep(1, length(x)), -1*eye)

mat2 <- cbind(x, rep(1, length(x)), eye)

mat <- rbind(mat1, mat2)

dir <- c(rep("<=", length(x)), rep(">=", length(x)))

rhs <- c(y, y)

types <- c(rep("C", length(x)+2))

max <- F

res <- Rglpk_solve_LP(obj, mat, dir, rhs, types = types, max = max)

yhat <- res$solution[1]*x +res$solution[2]

lines(x, yhat, col='green')

}

Regression using L1, L2 and L∞ norms source.

How do these implementation work? What are their limitations?